The outbreak of COVID-19 and the results of the pandemic on the worldwide monetary system are making consumers worldwide nervous about their funds. Analysis current these fears are heightened correct now, nevertheless anxiousness about managing funds isn’t a model new feeling for US consumers, in response to a Fb IQ survey carried out sooner than COVID-19 began to unfold broadly in america.

We’re all happy to assume that in order to grow a successful mobile game (or app) you need:

The survey found that folk want financial knowledge that will help them confidently deal with their money and attain their financial targets. They’re seeking reliable, dependable financial knowledge delivered in quite a few strategies—significantly now with digital collaborating in such an crucial place in every day lives. This need for clear and reliable knowledge presents a priceless different for financial suppliers institutions to work together consumers and assemble relationships. Considerably all through this time of social distancing, digital platforms is likely to be environment friendly in connecting producers and customers and delivering priceless knowledge to consumers the place they’re.

Producers can create and ship a wide range of knowledge by way of completely totally different avenues, akin to on-line groups, messaging or reside question-and-answer boards that allow consumers to digitally work collectively one-on-one reside with specialists. Resulting from digital platforms, these one-on-one interactions not ought to occur nostril to nostril.

To help entrepreneurs understand the financial behaviors and education desires of US adults, Fb IQ commissioned Viewers Concept and Ipsos to survey 1,000 primary inhabitants consumers, every people who have monetary establishment accounts and people that don’t, ages 18 and over. The survey occurred in November and December 2019, and its data reveals consumers’ targets and fears, the place they flip for advice and the way in which producers can engage to win their enterprise—knowledge that is merely as associated in the middle of the COVID-19 pandemic as a result of it was sooner than and can doubtless be after.

Many people proceed to have issues about reaching their financial targets

As we converse’s US consumers are more likely to have the similar financial targets as earlier generations: They should carry on value vary, have the power to cowl large payments akin to education and child care, put away some money for emergencies and enormous purchases and save for retirement.

Even sooner than the COVID-19 pandemic put an added stress on the monetary system and plenty of people’s non-public earnings, the survey found People had been concerned regarding the potential to reach these targets: Solely 35% of US respondents acknowledged they’d been positive their financial targets are attainable.

When the survey was carried out, respondents acknowledged their anxiousness was pushed by a wide range of issues, along with issues about monetary and political instability, the rising value of dwelling and rising debt fueled by payments akin to effectively being care. Add totally different components, akin to worries over needing to doubtlessly restart a career, working earlier retirement age and a means of vulnerability when dealing with financial institutions, and it’s easy to see why people are fearful about their financial futures.

Clients’ fears had been moreover pushed by how they view their financial state of affairs: Some 61% expressed concern with their potential to local weather a giant, stunning expense, and 59% expressed concern with their potential to supply for themselves and their family—a worry significantly prevalent amongst ladies1 and youthful adults.2

In reality, with completely totally different ages come completely totally different expectations and fears. Clients ages 18–34 had been further extra more likely to say they weren’t assured about their potential to deal with their non-public funds, and they also had been further extra more likely to particular worry about being able to current for themselves and their households. Youthful consumers had been moreover further concerned about being unable to buy a home, pay for education and afford child care.

“In the mean time, I’m in debt for my pupil loans,” acknowledged a 23-year-old man. Adults 35 and older, within the meantime, had been further extra more likely to say they’d been frightened about lagging in retirement monetary financial savings and being confronted with a sudden medical emergency that can eat into their monetary financial savings.

“I don’t save ample,” acknowledged one respondent, a 45-year-old woman. “I’m getting further into saving for retirement, nevertheless life goes by fast. It’s a long-term goal on account of I’ve loads of credit score rating stuff to scrub up first.”

What would put an end to these fears? Attaining financial effectively being. For nearly all of respondents, all through generations, that entails having financial stability, being prepared for a financial emergency, being self-sufficient and having non-public comfort/freedom.

How do consumers measure financial effectively being?

Financial institutions have an opportunity to supply a path to financial effectively being—and consumers pays consideration

What kinds of financial knowledge do consumers want? Each expertise has its private distinctive pursuits that mirror the place its members are in life.

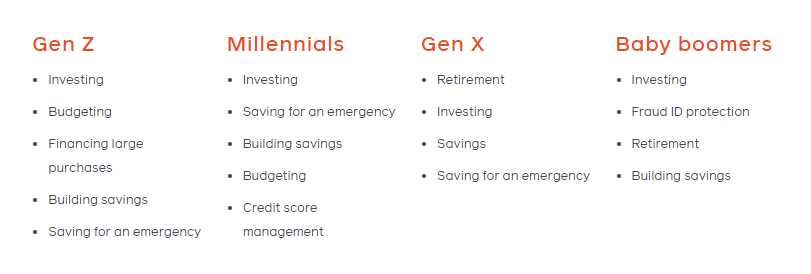

Credit score rating ranking administration is the financial matter members of Gen Z acknowledged they’d been most eager on learning about. Millennials want to seek out out about taxes and financing large purchases. Gen Xers are eager on retirement advice and knowledge, as are youngster boomers, who moreover acknowledged they want further particulars about fraud ID security.

This doesn’t suggest curiosity in issues is barely confined to explicit generations. The reality is, people of all ages acknowledged they should research further about virtually all issues, with youthful consumers significantly extra more likely to particular broad financial curiosity. This suggests financial service suppliers can attain a big viewers by overlaying a wide range of issues.

What issues had been generations most eager on?

By means of how consumers have to acquire financial knowledge, they acknowledged they’re open to many varieties. With the power to work collectively one-on-one with a person and ask questions in precise time is especially valued, with respondents displaying above-average curiosity in reside Q&A intervals with specialists and reside video calls.

In an increasingly digital world, financial institutions can meet people the place they’re: on-line groups and messaging apps

Some 47% of respondents ages 18–34 acknowledged their household and pals are the sources they perception most likely probably the most for financial knowledge.

These youthful consumers acknowledged they’d be cozy using on-line groups and messaging apps for finding financial advice and knowledge, considerably if others of their social circle are using these channels.

US consumers ages 18–34 are 1.3 cases further probably to utilize Fb for financial content material materials if their household and pals obtain this. Youthful consumers are moreover significantly fascinated about Fb groups that current financial content material materials, with 58% of people ages 18–34 expressing curiosity, in distinction with 46% of people ages 35 and older.

Common, 42% of respondents acknowledged they’re eager on personal groups to alter and share financial knowledge and advice. These are significantly widespread amongst ladies, with 51% expressing curiosity (as compared with 32% of males). Groups run by like-minded pals, akin to household and pals, are moreover a most popular risk for connecting with knowledge.

Receiving financial education by the use of messaging moreover resonates with consumers, considerably with youthful audiences: 61% of US consumers ages 18–34 acknowledged they’re cozy receiving financial knowledge over chat or a messaging app, and 58% say they’re cozy receiving financial advice this way.

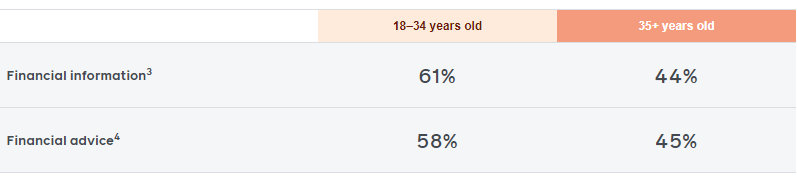

How cozy had been US consumers with receiving financial knowledge and advice over chat or messaging apps?

Financial institutions that moreover use these methods to work together with audiences would possibly uncover they’re able to entice further consumers to their conversations.

What it means for entrepreneurs

-

Current an understanding of consumers’ financial fears.

Of us normally have comparable broad financial worries—akin to being able to get financial financial savings and provide for themselves and their households. By demonstrating they understand these nuances and are an ally trying to find consumers’ best pursuits, financial institutions can assemble affinity with consumers.

-

Create avenues for people to connect reside with specialists digitally.

There could also be loads of curiosity for virtually all kinds of financial issues, significantly amongst youthful audiences. By creating a wide range of insights, considerably by way of methods that allow for reside interactions on-line, financial service suppliers can entice consumers to their conversations. Financial institutions must steadily verify these new inventive codecs to verify they’re deploying the perfect methods for reaching audiences.

-

One-on-one doesn’t ought to suggest face-to-face.

US consumers, significantly youthful ones, already flip to their household and pals for financial advice. This creates an opportunity for financial suppliers firms to utilize digital channels, akin to messenger, on-line groups and Fb, to connect with audiences. Considerably all through this time of social distancing, producers have an opportunity to leverage digital platforms that be a part of producers and consumers to ship priceless knowledge to consumers correct the place they’re.

Helpful useful resource: